The period leading up to the G20 meeting was generally marked by optimism and hopefulness. One commentator urged his readers: “Don’t write off the London G20 meeting. It could lay the foundations for fundamental global change, impacting currencies, gold and bond markets.”

On some level, the meeting probably did fulfill expectations. After only a few hours of discussions, the G20 agreed to “stricter limits on hedge funds, executive pay, credit-rating companies and risk-taking by banks. The summit also committed more than $US1 trillion to boost the resources of the International Monetary Fund and provide emergency cash to help distressed countries.”

Investors rejoiced and the markets rallied, with the Dow rising above 8000 points and capping “the best four-week rally since the week ending May 12, 1933.” Bulls can now retort that the stock market bust of 1929 took four years to recover, while the recession of 2008-2009 required less than one year. Forex markets also reacted “positively” to the G20 summit, lifting the Dollar above the important psychological barrier of 100 Yen/USD, and causing emerging market currencies to rise across the board.

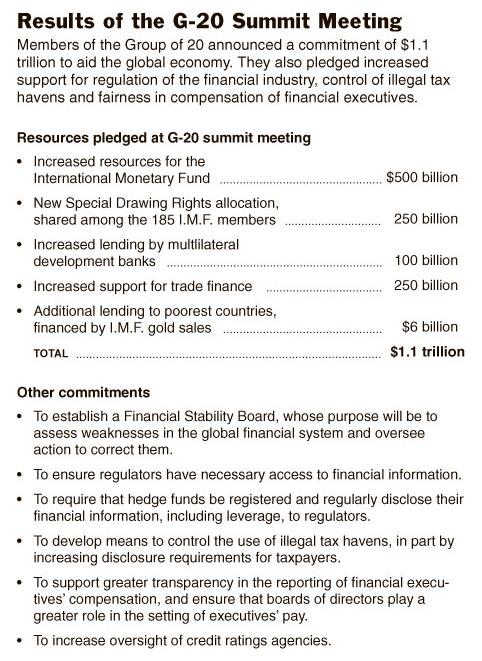

Monday, however marked a return to business as usual: “Post-G20 euphoria, which had helped to boost market confidence about a global recovery, proved short-lived as investors once again focused on the continued risks to the banking system.” It was probably only a matter of time before investors drilled beneath the surface of the impressive-sounding G20 rhetoric and large numbers, into the nuts and bolts of the summit’s policy prescriptions. [The chart below comes courtesy of the New York Times].

The headline-grabbing $1.1 Trillion figure, for example, is somewhat misleading. Over half of the $500 Billion “pledged” to the International Monetary Fund has either not been raised or not been explicitly authorized. Then, there is $350 Billion in trade credit, most of which is either redundant or double-counted, since “trade financing is rolled over every six months as exporters get paid for their goods and repay the agencies that lent them the money.” The remaining $250 Billion is accounted for in the issuance of IMF synthetic currency to member nations. However, given that the synthetic currency derives a significant portion of its value from the Dollar and Euro, this program cannot be effective if the US and EU opt out, of which there is a real possibility.

The summit also failed to meaningfully address concerns of the continued ole of the USD as the world’s de facto reserve currency. The expansion of the IMF synthetic currency program represents an important starting point, but at this point, it looks like China and the other supporters of an alternative system will have to wait for the next G20 meeting, to be held in September.

One commentator captured this frustration quite well: “The G20 Plan…tries very hard to preserve and perpetuate the existing US helmed global financial and economic order. An act of commission, on the one hand— buttressing the IMF— and an act of omission, on the other— remaining silent on the position of the US dollar— bear testimony to this.”

0 comments:

Post a Comment